Convergence and Resilience: The Total Portfolio Approach as the New Paradigm for Institutional Stewardship

The current institutional investment landscape is characterized by a profound dissonance between legacy frameworks and the structural realities of modern global markets. For seven decades, the architecture of institutional portfolios has been anchored in the foundational tenets of Modern Portfolio Theory (MPT) and its most tangible heir, Strategic Asset Allocation (SAA). This framework, while offering a historical sense of order and governance comfort, has increasingly become a source of systemic fragility. At Wind River Capital Strategies, the analysis indicates that the rigid silos of SAA - where asset classes are managed in isolation and rebalanced to static benchmarks - are fundamentally ill-equipped to navigate a regime defined by geopolitical fragmentation, structural inflation, and the blurring of lines between public and private capital.

In its place, a silent revolution is underway. The Total Portfolio Approach (TPA) has emerged as the superior alternative, transforming the portfolio from a collection of disconnected mandates into a single, dynamic organism oriented toward a unified mission. TPA is not merely a technical refinement; it is a holistic evolution of governance, culture, and risk management that treats the entire pool of capital as a integrated whole. This report details the mechanical and philosophical transition from SAA to TPA, providing a position on why this shift is mandatory for endowments, foundations, and public pensions seeking to maintain their fiduciary integrity in an era of heightened volatility.

The Structural Failure of Strategic Asset Allocation

The enduring appeal of SAA lies in its institutional utility. It provided a clear architecture for boards to exercise oversight and for consultants to measure manager performance. However, this clarity often masks a significant investment problem. SAA was designed for a more stable world where markets, risks, and capital flows were relatively predictable. In today's context, the assumptions underlying SAA have become constraints rather than safeguards. The separation of the "asset mix" decision from the "manager selection" decision creates inefficiencies, where the board sets a target weight for an asset class like "Real Estate" or "Private Equity," and the investment staff is then tasked with filling that bucket, regardless of the forward-looking attractiveness of the opportunity set.

One of the most damaging consequences of SAA is the breeding of internal "fiefdoms" or siloed behavior. When teams are incentivized to optimize their specific slice of the pie, they inevitably compete for resources and attention, often leading to unrecognized duplication of risk or disjointed exposures across the total fund. Furthermore, SAA's reliance on periodic, calendar-based rebalancing forces institutions to sell winning assets and buy laggards purely to maintain arbitrary weights. This "set-and-forget" mentality is dangerously slow to respond to regime shifts, as seen in the failure of traditional 60/40 portfolios during the inflationary shocks of 2022–2024, when the negative correlation between stocks and bonds - the bedrock of SAA diversification - completely disintegrated.

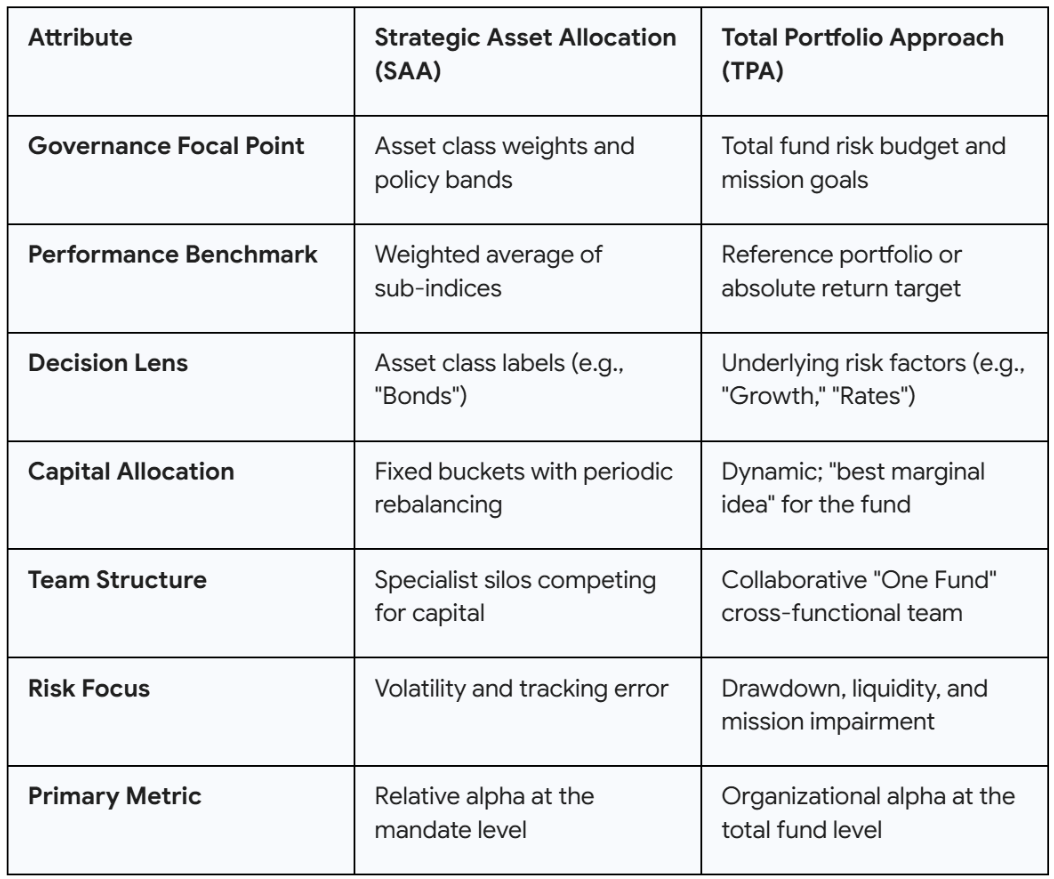

Comparative Framework: SAA vs. TPA Architecture

The movement toward TPA is driven by the realization that asset class labels such as "infrastructure" or "real estate" do not sufficiently capture the underlying factors influencing risk and return. TPA flips the governance model by bringing efficiency to portfolio design, though it requires a more "stretchy" and sophisticated approach to governance from the board.

The TPA Performance Edge: Harnessing Organizational Alpha

The shift to a total portfolio mindset is not a theoretical exercise; it is backed by compelling empirical evidence. Research from the Thinking Ahead Institute’s Global Asset Owner Peer Study reveals that adopters of TPA have achieved an average performance edge of 1.3% per annum over SAA adopters over a ten-year period. This outperformance is the result of what is termed "organizational alpha" - the value added through superior dynamism, better risk integration, and the elimination of redundant costs.

Under TPA, success is redefined. Instead of striving to beat an artificial policy benchmark that is often lagged and poorly constructed, the fund focuses on achieving its ultimate long-term objectives, such as a real return target or meeting payout obligations. This subtle shift has profound implications: it frees the Chief Investment Officer (CIO) to allocate to an unconventional or "esoteric" mix of assets if it better achieves the end goal, without the constant fear of "tracking error" relative to a sub-index.

The TPA framework is characterized by a "competition for capital" where every investment opportunity - regardless of its label - must earn its place in the portfolio by improving the total mix's risk-return profile. This allows capital to flow to where the risk-adjusted returns are highest in real-time. For example, if private credit offers superior yield and risk characteristics compared to public equities, a TPA-oriented fund can shift capital into credit without being constrained by a 10% allocation cap set years ago by a board.

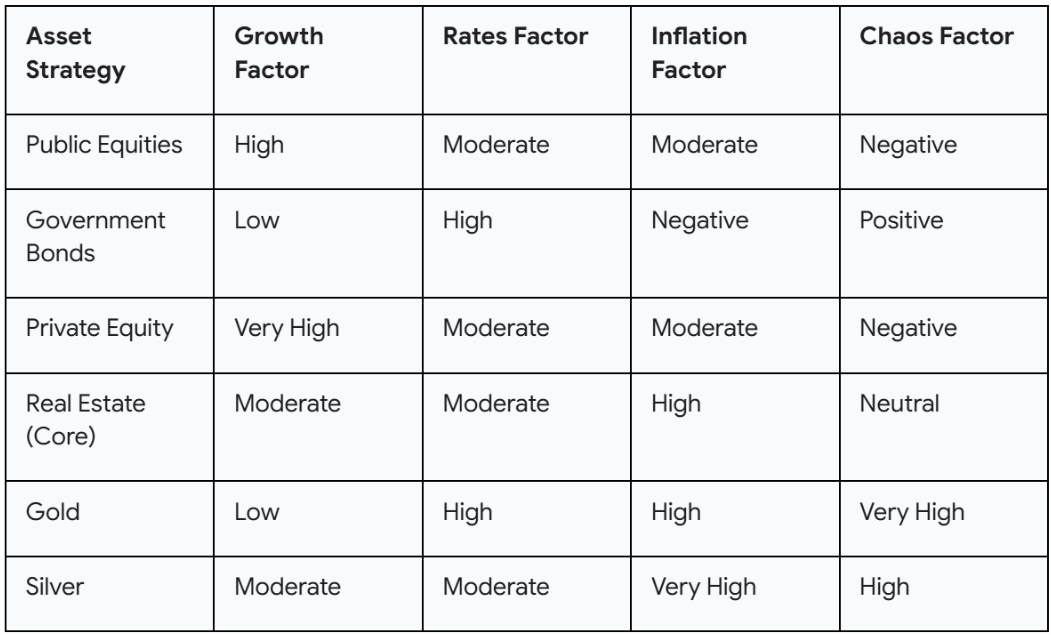

Factor-Based Risk Decomposition: Looking Through the Labels

The core technical innovation of TPA is the transition from asset space to risk space. Leading institutions like CPP Investments and GIC have moved beyond broad labels to analyze the fundamental economic exposures that drive their global holdings. By decomposing every asset into its constituent risk factors, a CIO can identify hidden correlations and ensure the portfolio is truly diversified across economic regimes.

For illustrative purposes only, we identify five primary risk factors that could define a hypothetical institutional lens:

Economic Growth: The exposure to global equity risk and business cycle expansion.

Real Rates: The sensitivity to changes in inflation-adjusted interest rates.

Inflation/Currency Debasement: Protection against the loss of purchasing power.

Liquidity: The premium earned for holding assets that cannot be immediately sold.

Chaos/Systemic Risk: A defensive factor designed to protect capital during "black swan" events.

This factor-based approach allows for a more robust stress testing of the portfolio. While an SAA framework might suggest a portfolio is diversified because it holds both "real estate" and "equities," a factor lens might reveal that both are highly sensitive to the same "growth" factor, leaving the institution vulnerable to a simultaneous drawdown.

Factor Exposure Mapping (Illustrative)

The TPA framework allows the CIO to adjust these factor dials dynamically. In a world characterized by fiscal irresponsibility and monetary expansion, the "Inflation" and "Chaos" factors must be elevated. This is where the strategic and tactical allocation to precious metals demonstrates the superiority of TPA.

Gold and Silver: The TPA Tactical Advantage in Practice

The regimes of 2025 and 2026 provided a definitive test case for how TPA allows for more effective positioning than SAA. In a traditional siloed model, gold is often relegated to a 2% or 5% "alternative" bucket, frequently capped by boards who view it as a non-yielding relic. A TPA framework, however, evaluates gold and silver as structural anchors and alpha engines designed to mitigate mission impairment during periods of systemic stress.

Gold as a Chaos Hedge and Strategic Anchor

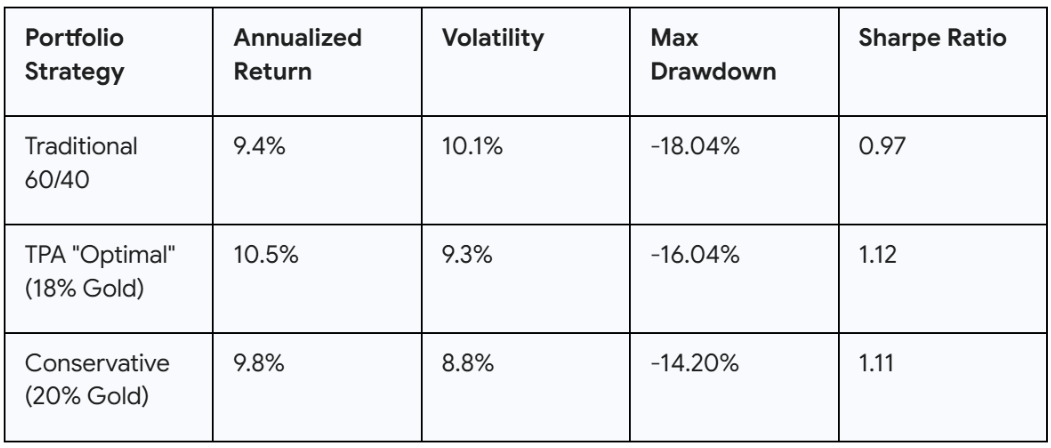

Academic and institutional research consistently points toward an "optimal" gold allocation that is significantly higher than what is found in most institutional portfolios. From 1973 to 2024, the Sharpe ratio of a traditional 60/40 portfolio was 0.97. However, an "optimal" portfolio that included an 18% allocation to gold increased the Sharpe ratio to 1.12 while simultaneously reducing the maximum drawdown.

Gold’s primary utility within a TPA framework is its near-zero correlation with equities (0.01), a characteristic that persists even during market crises when other correlations tend to converge to 1.0. At Wind River Capital Strategies, we view gold as a "pure" asset - it is one of the few institutional holdings with no corresponding liability, meaning it exists outside the dependencies of the traditional financial system.

Institutional Outcomes of Gold Inclusion (1973–2024)

In a TPA environment, the decision to hold gold is not a "bet" on price, but a strategic decision to buy insurance for the total fund. An SAA manager might be forced to sell gold after a strong price rally to maintain a 5% cap; a TPA manager, recognizing the rising "Chaos" risk factor in late 2025 due to geopolitical uncertainty and new tariff regimes, would have the flexibility to maintain or even increase the position, capturing the subsequent rally to $5,000 and beyond.

Silver: The "Availability Discovery" Regime

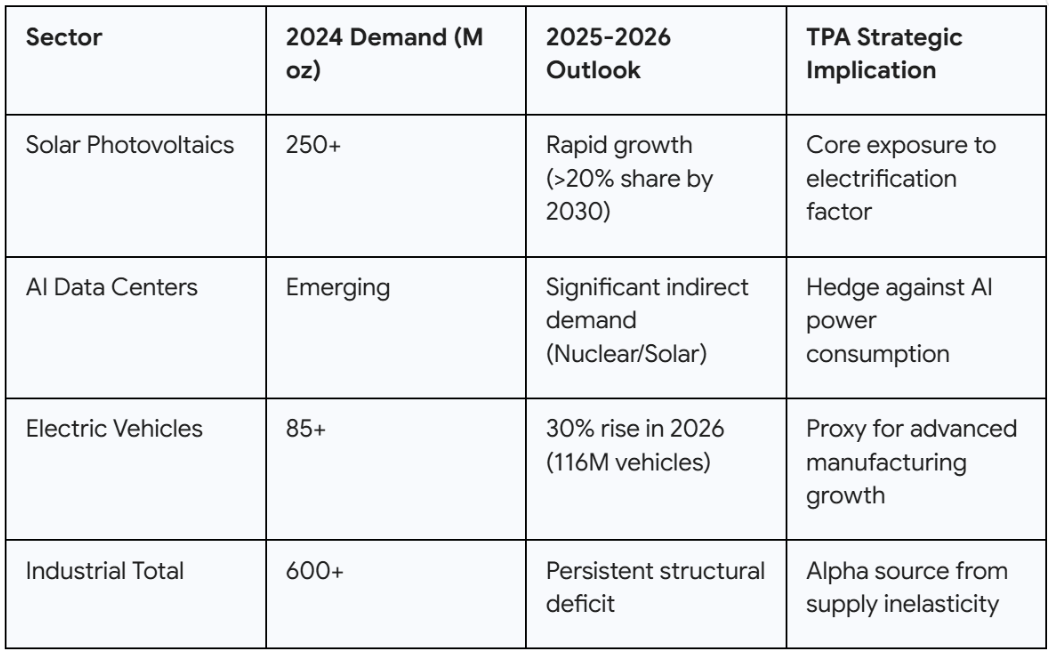

Silver provides an even more stark example of TPA’s tactical edge. Unlike gold, which is primarily a monetary asset, silver is a hybrid with massive industrial tailwinds. In 2025 and 2026, the silver market entered a regime of structural scarcity. Demand from the solar PV sector reached record levels, with solar panels consuming over 25% of annual global supply in 2024 and approximately 448 million ounces in the first half of 2025 alone.

A TPA-oriented team, utilizing cross-asset expertise, could have identified the "Availability Discovery" phase earlier than a siloed commodity desk. While an SAA framework might classify silver as a volatile commodity to be avoided, a TPA lens would recognize it as a play on several key factors: "Inflation," "Green Energy Growth," and "Industrial Scarcity".

Silver Demand Dynamics: 2024–2026 Forecasts

The "absurd" 190% move in silver from late 2025 through early 2026 was largely driven by these structural imbalances combined with momentum. A TPA framework allows for a "dynamic rebalancing" that captures these parabolic moves. Because TPA funds are measured against fund-level goals rather than a commodity index, they can hold outsized positions in silver when the fundamental deficit is high and the "Chaos" factor is rising, as witnessed in the January 2026 price spike to over $115 per ounce.

Governance as the Critical Enabler: The Role of the Reference Portfolio

The transition to TPA is as much a cultural transformation as it is a mathematical one. Successful adopters, such as the New Zealand Superannuation Fund (NZ Super) and Canada Pension Plan (CPP) Investments, emphasize that clear governance is the most critical ingredient. Without clear decision rights and a unifying benchmark, the flexibility of TPA can lead to confusion or unchecked risk-taking.

The Reference Portfolio vs. The Policy Portfolio

To solve the governance problem, TPA adopters typically use a "Reference Portfolio" - a simple, low-cost, notional portfolio of liquid equities and fixed income (e.g., 70% global stocks, 30% bonds) that aligns with the institution's risk appetite and time horizon.

The Reference Portfolio: Serves as the board's expression of risk. It is not managed; it is a passive benchmark used to evaluate the success of the investment team.

The Policy Portfolio: This is the actual, diversified portfolio built by the investment team. It deviates from the Reference Portfolio to capture alpha, harvest illiquidity premiums (via private equity or real assets), and tilt toward factors like precious metals.

This separation allows the board to focus on the "what" (the risk appetite) while granting the investment staff the freedom to manage the "how" (the tactical and strategic implementation).

Case Study: GIC’s Total Portfolio Framework

GIC Singapore manages the nation's reserves through a disciplined TPA that divides the fund into two distinct return streams:

Policy Portfolio: Focuses on harvesting beta and systematic risks. It is the long-term anchor of the fund.

Active Portfolio: A multifaceted overlay of alpha strategies. Every active strategy is "funded" by selling a slice of the Policy Portfolio. For a strategy to be retained, it must generate a return that exceeds its cost of capital (the funding beta) plus the additional risk taken.

This "competition for capital" ensures that every active bet - whether in silver futures or private equity buyouts - is held to a rigorous standard of performance relative to the total fund's objectives.

Managing Illiquidity and the Denominator Effect

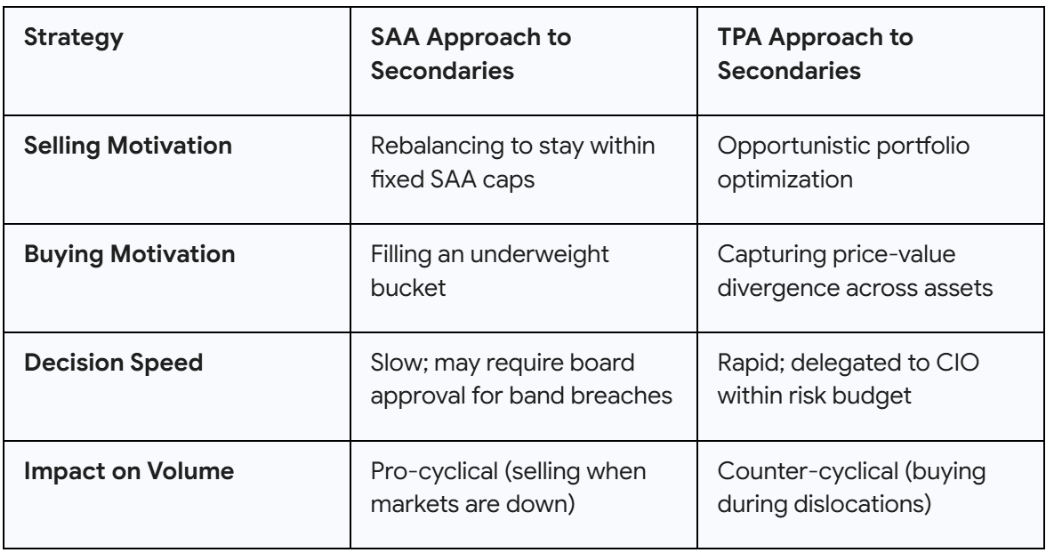

One of the most significant advantages of TPA for endowments and foundations is its superior management of private market exposures. Under traditional SAA, when public markets experience a sharp decline, the percentage of the portfolio held in private equity and real estate automatically spikes. This "denominator effect" often pushes institutions above their board-mandated SAA caps, forcing them to become "forced sellers" in the secondary market at the exact time when liquidity is most expensive.

A TPA framework views illiquidity through a different lens. Instead of compliance bands, it focuses on "opportunity cost" and "total fund resilience". If public markets are selling off, the TPA manager recognizes that public equities may now offer a higher forward-looking risk-adjusted return than some private holdings. This allows the fund to act with agility - either by pausing commitments or by opportunistically buying secondaries - without being "handcuffed" to legacy targets.

Research indicates that TPA adopters tend to have higher overall allocations to private markets because their governance structure allows them to tolerate temporary breaches of allocation thresholds in exchange for capturing long-term premiums.

TPA in the Secondary Market: From Compliance to Opportunity

The Internal Infrastructure: AI and Data as a Single Lens

Implementation of TPA requires a radical upgrade in internal information systems. Most institutional accounting systems are designed for record-keeping, not for a unified "investment lens". To successfully manage a total portfolio, the investment team must be able to see through to the underlying risk factors of every holding in real-time.

At Wind River Capital Strategies, we advocate for a "One Fund" technology strategy that integrates data from public markets, credit, private equity, and real assets into a single risk engine. This requires moving away from third-party commercial models that are often "black boxes" and toward internally tailored models that allow for faster adaptation to market conditions.

The use of AI is central to this platform. By automating the factor decomposition and stress-testing processes, the investment team can simulate "what happens if we shift $100 million from investment-grade bonds to physical silver?" across hundreds of scenarios for volatility, drawdown, and recovery resilience.

3D Investing: Integrating Risk, Return, and Impact

The TPA framework is uniquely suited to the emerging trend of "3D Investing," which integrates risk, return, and real-world impact into a single decision-making framework. For endowments and foundations with missions related to climate change or social equity, TPA allows these goals to be made "investable" at the total portfolio level.

Instead of a siloed "ESG bucket," TPA allows the institution to evaluate how every asset contributes to the fund's broader purpose. For example, a TPA fund might increase its silver allocation not just for its "Chaos" hedge properties, but as a strategic commitment to the electrification and green energy infrastructure that silver facilitates. This alignment of governance, culture, and portfolio construction ensures that the institution's values are woven into its investment DNA rather than treated as an afterthought.

Conclusion: The Mandate for Change

We stand at a moment of profound financial dissonance. While the surface of the market often appears calm, a forensic look beneath revealed a fracturing foundation. Valuation extremes in U.S. equities, coupled with structural deterioration in credit and the "circular" funding mechanisms of the AI era, have created a "Structural Bull Market Built on a Cyclical Precipice".

For the leadership of an endowment, foundation, or pension fund, the path forward requires a leap of faith to challenge business-as-usual. Strategic Asset Allocation, while comfortable, has become an anchor in a rising tide of complexity. The Total Portfolio Approach offers a way to regain control, to move with the market rather than against it, and to achieve the "organizational alpha" that differentiates the world's most resilient funds.

Actionable Positioning for the Institutional CIO

Abolish the Silos: Reorganize the investment team into a unified "One Fund" culture where incentives are tied to total fund success, not mandate-level benchmarks.

Adopt a Reference Portfolio: Clarify the board's risk appetite with a simple, liquid benchmark and delegate the implementation to the investment staff.

Implement Factor-Based Risk Management: Invest in the technology and AI infrastructure required to see through asset labels to the underlying economic drivers.

Strategic Deployment to Precious Metals: Increase structural allocations to gold and silver (targeting a combined 15–20% range) to hedge against currency debasement and capture the structural deficit in industrial metals.

Leverage Illiquidity: Use the flexibility of TPA to avoid being a forced seller during denominator effects and instead act as a strategic provider of liquidity in private markets.

The 1.3% annual outperformance of TPA adopters is more than just a number; it is the difference between an institution that merely survives and one that flourishes. At Wind River Capital Strategies, we believe that the "Quiet Revolution" of TPA is the defining challenge of the coming decade. The future belongs to those who view their portfolio not as a collection of parts, but as a single, resilient whole.

We would be honored to serve as a resource for your organization. Contact us today to discuss:

Contact | Connect with Financial Experts — Wind River Capital Strategies